Market Stats

March 2023 Stats

January 2023 Stats

Year over year stats are included for your review. Median sale prices continued to rise in 2022 over 2021 in our area!

If you are considering selling and/or purchasing a property, what does the Spring look like for timing? Well, the market remains strong although we have moved toward a balanced market which is a good thing, and this should continue. The Spring months will depend on the amount of inventory vs. the number of buyers prepared to purchase. Interest rates are predicted to rise again, however, this should not have a negative impact on sellers of waterfront property where funds can be discretionary. Single-Family detached homes not on water in our area are still more affordable than homes in the GTA. Unfortunately, higher interest rates always effect our kids who are first time home buyers.

If you have any questions regarding your affordability of selling / moving … please reach out and I will respond as quickly as I can.

September 2022 Stats

SINGLE FAMILY – Waterfront & Non-waterfront

YEAR OVER YEAR COMPARED TO 2021

ALMAGUINAverage sale prices have remained strong averaging a year over year increase between 15% - 18% for waterfront properties when compared to 2021, non-waterfront properties averaging a year over year increase between 12%-17% when compared to 2021.

The number of waterfront sales have decreased year over year when compared to 2021 by 47% with the average days on market remaining the same at 14 days. Non-waterfront sales have also decreased by 31% with the average days on market increasing to 19 from 15 in 2021

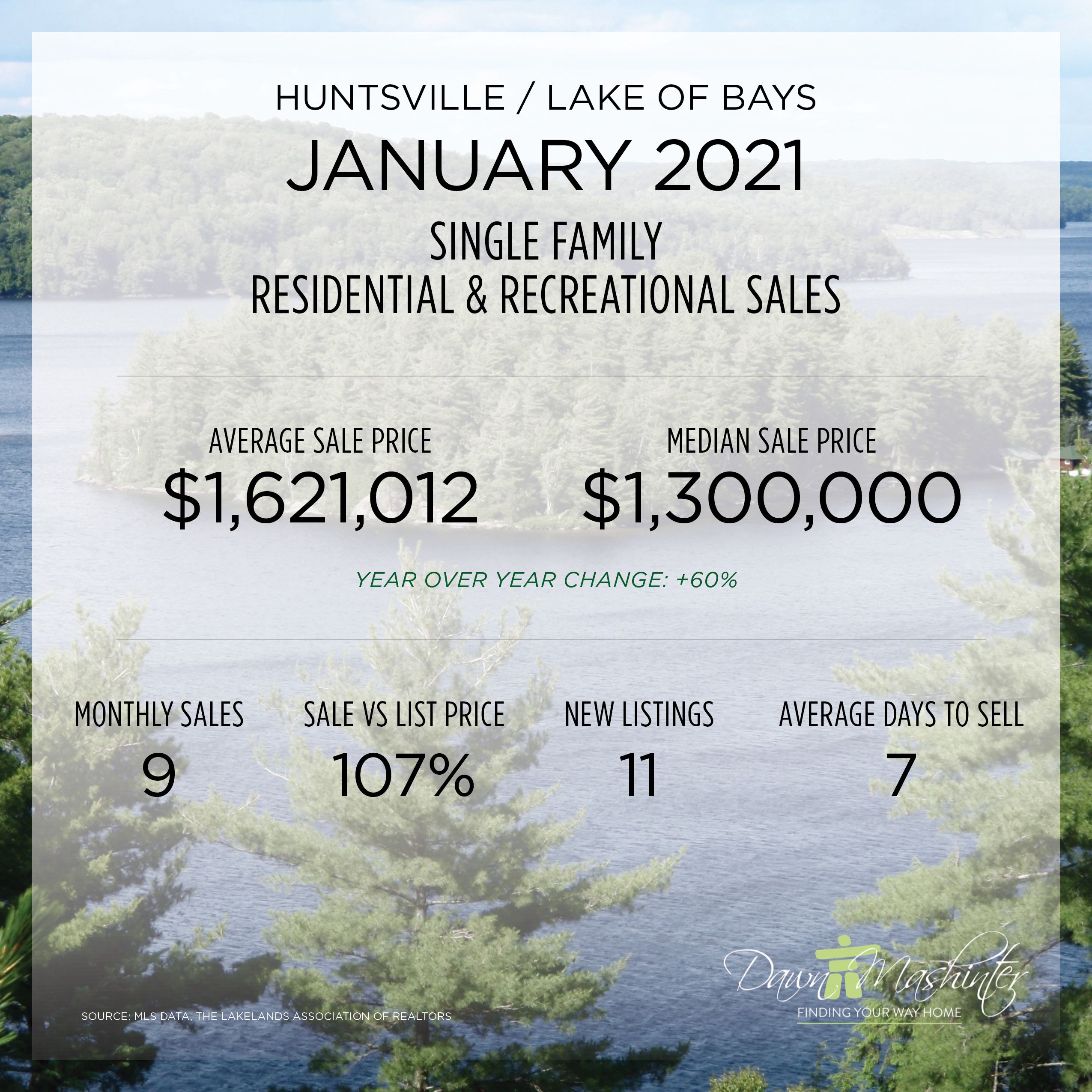

HUNTSVILLE & LAKE OF BAYS

Average sale prices have remained strong in this market as well, averaging a year over year increase between 12%-15% for waterfront properties when compared to 2021, non-waterfront properties averaging a year over year increase of 9% when compared to 2021.

The number of waterfront ales have decreased year over year when compared to 2021 by 53% with the average days on market increasing to 17 from 11 in 2021. Non-waterfront sales have also decreased by 47% with the average days on market up to 13 from 11 in 2021.

September 2022 sales below.

July 2022 Stats

Single-Family Detached Home Sales

Approximately 50% of new listings are selling within 30 on days the market, with the balance sitting on the market. Again, pricing is the key in this market, we now have more inventory to compete against.

Median sale prices continue to rise in the Huntsville & Lake of Bays area for both waterfront and non-waterfront properties when compared to July 2021 and to June 2022.

The Almaguin area median sale prices have decreased when compared to July 2021 and to June 2022 for both waterfront and non-waterfront properties. However, the 23 sales reflect lower priced properties.

The Fall market will begin soon! If you are thinking of selling, I would seriously consider selling now, we are not sure what the market will look like for 2023.

June 2022 Stats

Single-Family Detached Home Sales

The average and median sale prices continue to be higher when compared to June 2021. The exception is non-waterfront homes in the Huntsville and Lake of Bays area which took a bit of hit this past month.

Properties continue to take longer to sell when compared to the first quarter this year and multiple offer scenarios are no longer the norm.

Bottom line it is still a sellers-market if your home is priced correctly.

May 2022 Stats

May Single Detached Home Sales

Homes are now taking longer to sell on average, we have more inventory, however, still not enough inventory to move us to a balanced market.

Waterfront average sale prices have softened slightly but still remain strong and non-waterfront average sale prices in Huntsville continue to rise.

If you are thinking of selling, now is the time... we anticipate a balanced market in the Fall and possibly a buyers market in 2023.

Please feel free to reach out for more information.

The good news is that inventory continues to be low so if you are priced to sell you could still see a multiple offer situation.

Pricing is key.

April 2022 Stats

It is still a seller's market!

Sale price averages continue to rise on year over year average. We are still seeing some multiple offer situations, however, there are not as many buyers looking to move north or invest due to the volatility of the stock market and higher interest rates.

The good news is that inventory continues to be low so if you are priced to sell you could still see a multiple offer situation.

Pricing is key.

March 2022 Stats

Single family home sales have increased when compared to last year. However, average and median sale prices have decreased since February. Let's wait and see what April sales look like and pick it up from there.

February 2022 Stats

REAL ESTATE MARKET REPORT

Muskoka has been labelled one of the hottest markets for 2022. After seeing increases between 40-75%* since the start of the craziness in 2020 (depending on where you call home), there is talk of another 20% increase for 2022. Sellers will rejoice in this news and benefit from the surge in demand. Investors and buyers from southern centres will continue to drive the market. Please note that we had no waterfront sales in Huntsville and Lake of Bays for the month January to report due to lack of inventory!

The Real Estate market activity in 2021 was nothing short of remarkable considering the highs we saw in 2020. December waterfront home sales cooled slightly, but were still close to what we would expect in a typical December, while non-waterfront properties were still well above average for this time of year. In both cases the number of newly listed properties were unable to keep pace with the number of sales. Subsequently, overall inventory fell in both categories and were sitting at new record lows. The lack of supply combined with the current level of demand drove average prices in both waterfront and non-waterfront properties to new all-time highs in December. Overall, the market balance is still firmly in favour of sellers and without an influx of new listings, it is reasonable to expect that the current market conditions will continue well into Q1 of 2022.

January 2022 HOME SALES

NOVEMBER 2021 HOME SALES

OCTOBER 2021 HOME SALES

SEPTEMBER HOME SALES

Single Family Detached Homes on Water and off Water

The average sale pice is up when compared to August and up when compared to September 2020. We are still seeing multiple offer situations if properties are price accordingly.

August 2021 Stats

The lack of inventory and the reduced time on the market have created a little bit of a "hurry up and wait" scenario. Our months of inventory in 2021 never crossed 2% as compared to a little over 4% last summer. With this, clients are often watching and waiting to jump at the next new listing that meets their criteria. The frenzy has died down while plenty of properties are still finding multiple offers and a decent percentage above list price. We peaked this year with sales at 109% of list price but "cooled" to an even 100%. It is nothing new to say that the market will depend very much on what happens with inventory levels.

JULY 2021 SALES

JUNE 2021 SALES

Waterfront sales continued to be strong throughout the month!

- HUNTSVILLE & LAKE OF BAYS Single family detached average sale price increased by 60% when compared to June 2020. The average selling price coming in at $1,654,450.

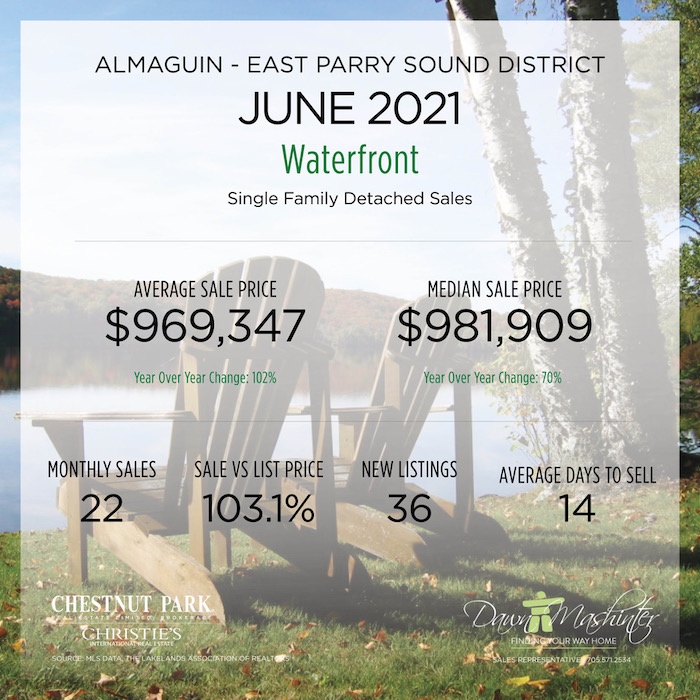

- ALMAGUIN / EAST PARRY SOUND DISTRICT Single family detached average sale price increased by a whopping 102% when compared to June 2020! Record breaking numbers here for sure. The average selling price coming in at $969,347 WOW! This demonstrates that buyers are willing to drive further north to get more for their buck, craving more greenspace for their property, and to purchase on less populated lakes.

Average day on market were 14-15 in both areas with the average list price to sale price ratio coming at 103.1% – 106.6%

Non-waterfront sales, Single Family Detached

- HUNTSVILLE & LAKE OF BAYS average sale price increased by 34% when compared to June 2020. The average selling price coming in at $732,009, taking 15 days on average to sell. List price vs. sale price ratio 102.2%.

- ALMAGUIN / EAST PARRY SOUND DISTRICT average sale price increased by 14% when compared to June 2020. The average median sale price coming in at $380,134, taking 28 days on average to sell. List price vs. sale price ration 98.4%

Interesting to note that our inventory increased in both area’s for both waterfront and non-waterfront single family dwellings when compared to June 2020, however, the selling prices continue to increase across the board consistently. We have noticed some change to non-waterfront property demand in the Almaquin area this past month, and we are now seeing conditional accepted offers and price decreases in the Huntsville area.

JANUARY 2021 – APRIL 2021: MUSKOKA AND ALMAGUIN (PARRY SOUND DISTRICT)

This report almost writes itself. The market forces that have driven recreational, secondary, and rural markets have remained unchanged through the pandemic. The desire for space in settings safer than dense urban centers coupled with the ability to work remotely have made these marketplaces a magnet for buyers. Historically low interest rates have also contributed. The combined effect of all these factors has resulted in a dramatic increase in demand, average prices and a decline in available inventory.

For all waterfront sales across the region, the median sale price increased by a stunning 67 percent on a year-over-year basis. The average sale price for waterfront properties in the region is now $850,000. This is an eye-popping number, particularly given the broad range of property values throughout the various sub-markets region. Here are some examples of what has happened to sales and prices in the region.

Waterfront property sales in the Almaguin area increased by a stunning 100% compared to the same period in 2020. Months of inventory declined from 11.25 months to 1.25 months. These sales results represent a new record for the region. Properties spent 11 days on the market, correspondingly the average sale price exceeded $800,000 versus $404,500 in 2020, also a new record!

Similarly, in Lake of Bays sales more than doubled over the same period compared to last year, again a record. Months of inventory declined from 26 months to 3.6 months. Properties spent only 12 days on market, and the median sale price came in at $1,027,000, a 14.2 percent increase on a year-over-year basis.

It is interesting to look at average sale prices on Muskoka’s three big lakes, Lake Muskoka, Lake Rosseau, and Lake Joseph. Unlike the other markets in the region, average sale prices have actually declined in the first four months of 2021. This is counterintuitive, given that the same economic factors are at play in the region. What has happened is that these economic factors have brought many buyers to the region seeking to purchase properties at lower price points and sellers have placed their properties on the market to be sold at exceptional prices. There has been no shortage of very high-priced sales, however, the plethora of “lower-priced” sales ($1,500,000 to $2,500,000) has brought the average sale price down dramatically.

More than 60 percent of recorded sales were in the $1 Million to $3 Million range. The big lakes are still the region’s most expensive market with 21 percent of all recorded sales for 2021 (38 properties) coming in at over $4,000,000.

Looking forward, we see market activity leveling in the Muskoka and region marketplace with, of course, sub-market differences. This is due to a number of factors. Firstly, as this report indicates, prices have reached unprecedented record levels, precluding some buyers, even with “city” money from engaging in the market. Secondly, the urgency for space and sanctuary driven by the pandemic has to some extent abated, due to people feeling safer as a result of the rollout of the vaccination program in Ontario, and thirdly, more inventory coming to market.

In May of 2020, 43 waterfront properties came to market. This May, 168 are now available to buyers. Year-to-date (January to May) 582 properties have come to market compared with only 483 last year, an increase of more than 20 percent.

This levelling should not be interpreted as a slowdown or decline in the market. Rather the edges of the frantic pandemic market have been smoothed over, resulting in a still very strong but less frenetic market landscape.

*SOURCE THE LAKELANDS ASSOCIATION OF REALTORS - MLS